2018 Edition

View the infographic

Datacap partnered with Piper Jaffray & Co., an investment bank and research firm, to conduct a payments industry survey that consisted of responses from an amalgamation of 404 Value-Added Resellers (VARs), Independent Software Vendors (ISVs) and Independent Sales Organizations (ISOs) who are all on the front line in forming today’s payments landscape.

The responses provided an intriguing look into the payments industry from the perspective of POS and payments providers.

Here’s what we found:

Survey Demographics

Our Survey respondents were comprised of…

- 60% – VARs

- 28% – ISVs

- 7% – ISOs

- 5% – Other

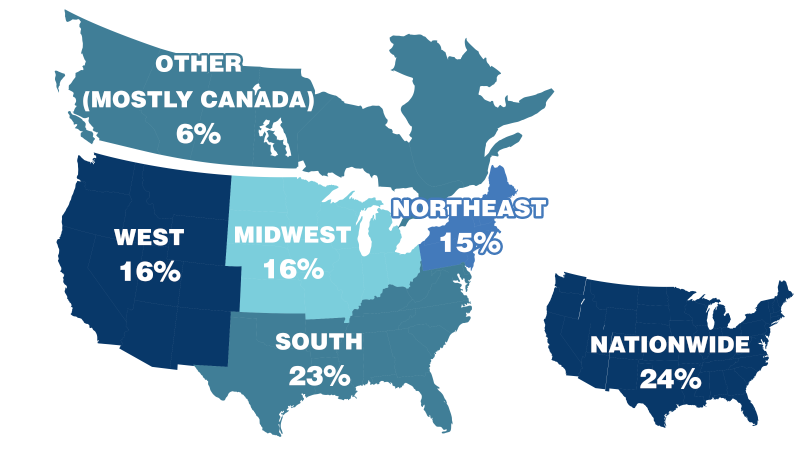

Geographical mix of VARs, ISVs, ISOs:

- 16% across the Midwest

- 15% across the Northeast

- 23% across the South

- 16% across the West

- 24% Nationwide

- 6% Other (Mostly Canada)

Integrated vs Non-Integrated payments

Our respondents said that 70% of their merchants use an integrated payment solution while 30% of their merchants identified using a non-integrated solution or stand-beside terminal.

Analysis:

We believe that because only 70% of respondents are implementing integrated payment solutions the remaining 30% represents a significant opportunity for forward-thinking Point of Sale providers.

Integrated Payments Adoption by industry Vertical

Our survey respondents most heavily serve the Restaurant, Retail, Entertainment, QSR, Hotels/Hospitality and Grocery industry verticals.

71%

Restaurant

69%

Retail

71%

QSR

68%

Grocery

74%

Entertainment

60%

Automotive

58%

Healthcare

65%

Electronics

69%

Hotels

63%

Petroleum

NEW VERTICAL

Unattended

NEW VERTICAL

Cannabis

Analysis:

New verticals such as unattended kiosk/self-checkout and cannabis provide new and unique opportunities for VARs-ISVs.

EMV Adoption Continues to Rise

Survey respondents reported that 50% of their SMB merchant bases have upgraded for EMV, which is a significant jump from the 35% reported in last year’s survey. VAR/ISV survey commentary highlighted continued demand to upgrade and certify SMB merchant POS hardware for new EMV-capable devices.

We expect this trend to not only continue, but to grow significantly now that EMV is widely available. This data implies that there is still significant opportunity to upgrade merchants to accept EMV, despite being three years past the liability shift.

EMV Adoption

Analysis:

Although EMV acceptance seems nearly ubiquitous three years past the liability shift, this data shows an obvious opportunity for upgrade revenue for POS providers.

VARs and ISOs tend to offer more than one Point of Sale Software Solution

Analysis:

The majority of VARs/ISOs offer three or more POS software solutions, so it’s important for POS ISVs to build attractive and profitable VAR programs to ensure that VARs lead with their solution when selling to merchants.

Recurring Revenue Opportunities Abound for Vars/isvs

Only 59% of VARs/ISVs offer a recurring revenue “as-as-service” model for their POS solutions to SMB merchants, unchanged from the 59% in 2017’s survey results. The other 41% currently use the break/fix or “one-time” sales model.

Survey responses indicate 22.8% of merchants are using Point of Sale obtained via an “as-a-service” model.

Analysis:

We believe this presents a massive opportunity for VARs-ISVs to migrate their merchants to a “as-a-service” model for their solutions to build recurring revenue.

Year-over-Year Growth expectations

The majority of our survey respondents indicated 2018 revenue growth expectations flat to +10% YoY (representing 58% of survey responses) with a median expectation in the MSD-HSD range.

Analysis:

We believe that VARs that have established some sort of recurring revenue either via a direct rental program or a processor-specific rental program are better able to predict growth patterns and ensure year over year growth.

Processor Partnerships

Processor Partnerships

- 41% of respondents partner with 0-1 processor

- 46% of respondents partner with 2-4 processors

- 13% of respondents partner with 5 or more processors.

Analysis:

We believe the 41% of VARs/ISVs using less than 2 processors represents a significant opportunity for VARs-ISVs to diversify their processor partnerships to allow flexibility for their merchants and to protect recurring revenue.

Processor OWNED Point of sale breeding competition

Only 20% of respondents were willing to work with a processor that sells or offers their own Point of Sale.

Analysis:

We believe that establishing a SAAS sales model and providing top-tier customer support helps VARs/ISVs compete with processor owned POS solutions. Additonally, we encourage VARs/ISVs to choose payments partners that have VAR programs without conflicts of interest.

Omnichannel Requests are growing

31% of SMB merchants have requested an omnichannel payment solution, where businesses can provide their customers with the ability to purchase goods and services through virtually all avenues: online, in person, by phone or through apps, among others with a seamless experience for each payment option.

Analysis:

This is still a relatively modest percentage, but it represents a increase from past surveys and an opportunity to provide additional value for your merchant base.

More VARs/ISVs are offering a Mobile POS Solution

60% of VARs and ISVs are offering a mobile POS solution today.

Analysis:

This represented a slight increase from our survey from last year, which implies that Mobile POS applications are continuing to gain in popularity in this space although there is plenty of room for growth.

Interest in POS upgrades is growing

75% of respondents reported stronger merchant interest in upgrading their POS software functionality.

Analysis:

EMV Pay-at-table, Offline processing, Mobile POS Extensions, Value-Added Services, and Enhanced Security Features are examples of upgrades merchants are considering.

Factors that drive VARs/ISOS to switch POS Providers

Respondents were asked to rank the following factors from 1-5, where 1 was the most important and 5 was the least important. POS software functionality remained the most important factor for VARs & ISOs when selecting POS software solutions from ISVs with 71% listing it as the #1 or #2 factor, which is the same percentage reported in last year’s survey. Price/resale margin was the second key factor.

POS Software Functionality

Price/Resale Margin

Service

Dealer-centric vs. Direct Sales Model

Program Changes after 3rd party acquisition

Other

Analysis:

POS software functionality remained the most important factor for VARs/ISOs when selecting POS software solutions. The remaining factors from most important to least important are: Service, Dealer-Centric vs. Direct Sales Model, and Program changes after 3rd party acquisition.

Digital/Cryptocurrencies gaining traction?

Only 8% of of merchant clients are requesting payment solutions to enable acceptance of digital currencies and cryptocurrencies like Bitcoin, Ethereum, Litecoin, etc.

Cryptocurrency Requests

Analysis:

While we believe the results are indicative of the tech’s novelty and the relative friction with crypto merchant payments, we continue to believe crypto based payments are not quite ready for universal adoption.

Information derived from survey of Datacap partners, conducted in conjunction with Piper Jaffray. The survey received responses from hundreds of Datacap’s VAR/ISV distribution partners for merchant processors operating in the integrated point-of-sale (iPOS) channel.