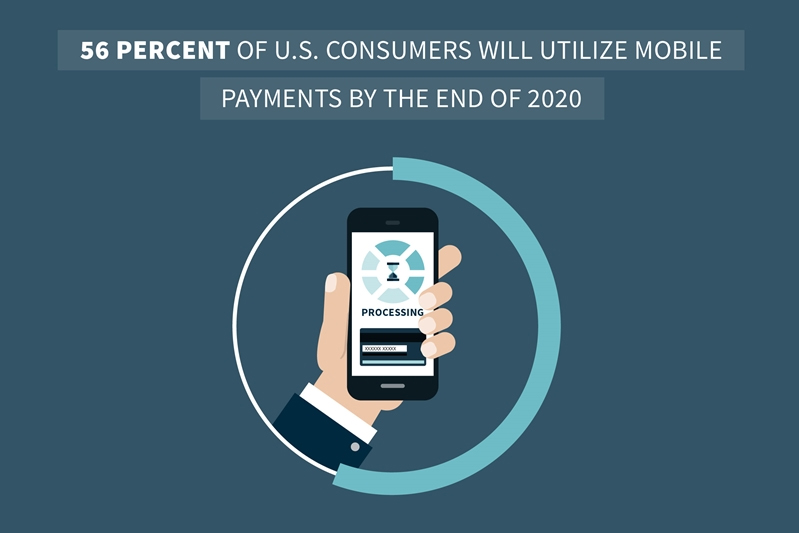

Consumer use of Mobile Payments by 2020

When the first iPhone came out in 2007, few merchants envisioned a world in which they would accept payments from smartphones. Now, anyone can use Apple Pay, Samsung Pay and other mobile payment apps to buy goods. The question is, are people actually doing so?

Rates of mobile payment adoption

There probably will be a time when most people pay with their smartphones, but that time isn’t going to arrive next year. BI Intelligence noted that the number of U.S. consumers making mobile payments will rise at a compound annual growth rate of 40 percent between 2016 and 2020. To be fair, that’s very healthy adoption, but that won’t mean an overwhelming number of Americans will place their complete financial trust in smartphones.

By BI Intelligence’s estimate, 56 percent of U.S. consumers will utilize mobile payments by the end of 2020. We’re not there yet. However, the researchers did find total mobile payment value would reach $75 billion in 2016. So it’s not as if people are abstaining from mobile payment apps entirely, it’s simply that adoption isn’t as ubiquitous as some would assume.

Consumer sentiment and behavior

When Apple Pay, Android Pay and other mobile payment apps arrived on the market, why didn’t consumers flock to them immediately? Based on its research, BI Intelligence speculated that most people are hesitant to abandon tried-and-true payment methods. It’s not that the mobile wallets are poor products. Rather, consumers simply aren’t that enthused about them.

Millennials, not surprisingly, may be the chief generation driving mobile payments adoption. In 2015, FICO conducted a survey of U.S. banking customers and found 32 percent of people between the ages of 18 and 34 said they would likely use mobile payment options. In contrast, only 16 percent of people aged 35 and older said they would do the same.

Mass adoption is coming, but not in dramatic form. The transition will be gradual, expanding as Apple, Google and other companies integrate more useful features into their mobile wallet products. More importantly, merchants must be able to accept payments via these mobile apps, and that’s where the challenge lies.

The challenges associated with mobile payments

Integrating mobile payments into existing operations introduces repercussions associated with security, device compatibility and EMV certification. Furthermore, implementing new POS devices that accept mobile payments into existing operations is a burden for merchants that lack the technology to streamline this process. The implementation of payments middleware is an excellent way to obtain plug and play support for mobile payments (and other functionality) across all payment processors.

With respect to data protection, mobile payments are not as risky as some would assume. A study from the Information Systems Audit and Control Association found some mobile wallets utilize tokenization. Instead of transmitting a card’s primary account number, they produce random tokens when interacting with POS terminals. In fact, ISACA discovered mobile payments’ tokenization features supersede security functions common in card-based transactions.

And when it comes to integrating mobile payment support, different POS devices bring distinct capabilities. While some offer near-field communication (NFC), others scan QR codes displayed on smartphone screens. These two technologies, while both within the realm of mobile payments, possess varied implications for in-store customer service, security and payment processing.

“150 million Americans will use mobile payments by 2020.”

EMV integration opens the door for mobile payments

Depending on how eager they are to serve the 150 million Americans who will use mobile payments in 2020 – as per BI Intelligence’s estimate – your clients may approach you to integrate mobile wallet-compatible devices into their operations.

First, assess their existing devices. Do they accept EMV cards? Most POS solutions that are compatible with chip cards also support NFC – especially systems that have utilized a competent payments middlware partner. In this case, NFC-based mobile payments should be part of a standard EMV upgrade.

What about the clients who do not have EMV PIN pads? Expedite the roll out with a payments hub. Payments hubs are plug-and-play solutions that come with built-in EMV certification to a variety of PIN pads. Utilizing HTTP posts, these hubs connect any POS application, regardless of operating system, to EMV-ready devices.

Preparing for the future isn’t a bad idea. Assess your client’s current infrastructure and customer demands, so that you can ensure that your produc toffering lines up with what merchants will be requring in the near future.