U.S. consumers have flirted with mobile payments for years, taking their time to adopt this technology that allows them to make in-person payments using their smartphones.

U.S. consumers have flirted with mobile payments for years, taking their time to adopt this technology that allows them to make in-person payments using their smartphones.

eMarketer reported that the number of U.S. consumers making proximity mobile payments is steadily increasing. Consumers using mobile wallets reached 64 million – about 29 percent of smartphone users — in 2019, up from 58.7 million in 2018. This puts the U.S. in sixth place when compared to proximity mobile payments use around the world, behind China, Denmark, India, South Korea and Sweden.

Reasons the U.S. is lagging in mobile payment adoption

U.S. adoption of mobile payments isn’t necessarily a sign that consumers are disinterested. A variety of factors have had an impact on mobile wallet use – which other countries didn’t encounter.

First is timing. While the rest of the world was discovering the convenience of mobile payments, the U.S. was focusing all of its attention on transitioning to EMV technology. Apple introduced Apple Pay in 2014, just one year before the EMV liability shift. Although by that time some merchants had upgraded their technology to EMV — in most cases also enabling them to accept contactless, mobile wallet payments — many more were delayed due to the software they used and their solutions providers’ schedules. Countries with newer payment infrastructure didn’t have to wait for upgrades to an older system before enabling contactless payments.

Another force to overcome in mobile payment adoption is the fact that people are creatures of habit. U.S. consumers are long-time plastic users, so mobile payment adoption requires changes in behavior, which isn’t true of consumers in all other countries.

Last but not least, another reason that mobile wallet adoption has progressed at only a modest pace is that not all merchants accepted them. Although the majority of merchants’ systems now have the capability to enable contactless payments, many have still not configured their systems or trained their teams for these types of transactions. Some of the initial excitement consumers had over mobile wallets waned when they realized they couldn’t use them everywhere.

What’s Not to Love?

Consumers who have adopted mobile payments are sold on the technology for several reasons:

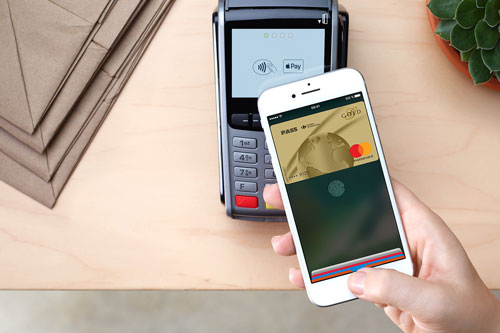

- Tap and go: Many mobile wallets use near-field communication (NFC) technology that allows a customer to open their app and just hold or tap their smartphone near a payment terminal to make a payment. Transactions are quick and easy.

- Security: Although there was some initial skepticism about the security of mobile payments, encryption, tokenization and other security technologies used in smartphones in combination with the same security used with EMV payments makes mobile payments very secure—even more secure than using a physical payment card.

- Less to carry: People usually have their smartphones with them. Using a mobile wallet can eliminate having to carry credit cards, loyalty cards, cash – and organizes everything in one app.

New Incentives to Use Mobile Payments

Even with the benefits of using a mobile wallet and growing merchant acceptance of contactless payments, consumers still – as with any technology – need a nudge to try it. In 2020, a perfect storm seems to be brewing that could have consumers reaching for their phones instead of their wallets when it’s time to pay:

- COVID-19: People have grown acutely aware of the health risks of handling cash or touching a PIN pad after someone else has used it. A mobile wallet is a form of contactless payment— no touch or shared devices required. This feature of mobile payments appears to have had an impact, at least in the short term. In April, Mastercard reported a 40 percent jump in contactless payments.

- More Gen Z consumers: Digital natives are becoming a larger part of the consumer population – and use their smartphones for everything from streaming and games to texting and video chats. They’re also mobile shoppers and comfortable with P2P payment apps. Gen Z shoppers are predicted to make up 59 percent of U.S. consumers by 2026, so an increase in proximity mobile payments may grow proportionately.

- Transit fares via contactless: The turning point in contactless payment acceptance in the UK was London’s transit agency upgrading to accept tap-and-go payments. Although delayed until the end of the year due to coronavirus, the New York Metropolitan Transportation Authority is implementing a contactless fare payment system, which will give millions of people the opportunity to use mobile wallets, see how convenient they can be, and incorporate them into their daily routine.

Make sure your clients are ready

The takeaway for solutions providers is to make sure your clients are ready when mobile wallet adoption grows. Once U.S. consumers are paying fares or buying groceries with mobile wallets, they’ll also want to use them at the fast food drive-up, at the salon, or at a repair shop. Integrating your solution with a full-featured omnichannel payments platform will ensure your clients can accept contactless payments – as well as the other forms of payment consumers want to use both in-person and online. As a trusted advisor, make sure your clients are prepared to meet this demand.